This patented system of clearing financial instruments is based on integration of commercially available cash management and flexible risk management. The system significantly advances the present practice of existing "self clearing" for select trading platforms. The system features multi-platform capability because of its flexible approach to risk management. The main advantage of the system is its stand-alone performance ( Node) as well as networking with all other Nodes anywhere in NAFTA area. This system has the lowest cost of clearing as compared to centralized clearing system.

Thursday, August 28, 2014

Wednesday, December 4, 2013

DISTRIBUTED CLEARING CONCEPT

THE ROLE OF PARTNER BANK IN DISTRIBUTED CLEARING THAT OCCURS BETWEEN TWO TRADING FACILITY (NODES)

Monday, August 27, 2012

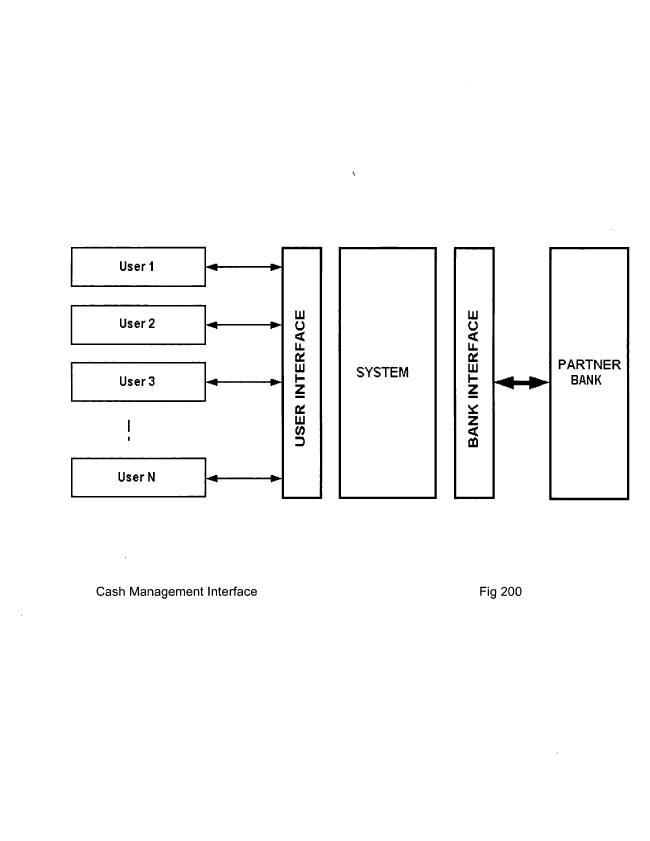

CASH MANAGEMENT FOR CLEARING SYSTEM

A CONCEPTUAL REPRESENTATION OF THE OPEN CLEARING SYSTEM WHERE THE USER'S TRADE EXECUTION IS CLEARED THROUGH BANKING SYSTEM

Decentralized Clearing of Financial Instruments

The existing central clearing houses are now confronted with an unpleasant choice of continuing with their role of order matching of traditional products at a competitive rates or trying to capture a new explosive over-the-counter (OTC) market albeit with drastic and therefore changes in their methodology.

The regulatory bodies are encouraging the OTC market participants to embrace some sort of clearing for price transparency and a means of risk management. The privileged classes of OTC markets, namely energy and financial industries will probably lose their present status of exemption from Commodity Futures Trading Commission (CFTC) rules and regulations in the near future forcing central clearinghouses to undergo the necessary and anti-monopoly type of changes.

While the idea of centralized clearing did-and still serves- the valuable purpose of mass and hence cheap way of clearing financial dealings, the nature of OTC market is by definition a largely clustered bilateral trades defying uniformity and centralization. Even, as in the case of energy market, the private central clearinghouses of Intercontinental Exchange (ICE) will not be able to attract any significant share of OTC market; neither will Bank of America with its newly introduced clearinghouse for OTC financial products.

The new concept that can truly address this challenge is a distributed intelligent self-contained clearing Node with full interconnectivity. This patented technology can be compared succinctly with the legacy of central clearing below.

The regulatory bodies are encouraging the OTC market participants to embrace some sort of clearing for price transparency and a means of risk management. The privileged classes of OTC markets, namely energy and financial industries will probably lose their present status of exemption from Commodity Futures Trading Commission (CFTC) rules and regulations in the near future forcing central clearinghouses to undergo the necessary and anti-monopoly type of changes.

While the idea of centralized clearing did-and still serves- the valuable purpose of mass and hence cheap way of clearing financial dealings, the nature of OTC market is by definition a largely clustered bilateral trades defying uniformity and centralization. Even, as in the case of energy market, the private central clearinghouses of Intercontinental Exchange (ICE) will not be able to attract any significant share of OTC market; neither will Bank of America with its newly introduced clearinghouse for OTC financial products.

The new concept that can truly address this challenge is a distributed intelligent self-contained clearing Node with full interconnectivity. This patented technology can be compared succinctly with the legacy of central clearing below.

Central Clearinghouse versus Open Clearing Node

a. complex general purpose design a. simple, efficient and configurable

b. high cost of operation, b. low cost and no maintenance

c. rigidity with respect to new application c. highly flexible

d. legacy, resisting change d. new concept, highly adaptable

e. high risk e.limited in scope and size

f. requiring high level management f. small team, minimum supervision

g. too many disparate parts g. seamlessly integrated

h. global reach through relationship h. real time inter-networked

k. no matching engine k. built-in

Specific Issues

a. Netting a. Distributed Node allows reporting of all transaction

b. Risk management b. Any algorithm /real-time mark-to market

b. high cost of operation, b. low cost and no maintenance

c. rigidity with respect to new application c. highly flexible

d. legacy, resisting change d. new concept, highly adaptable

e. high risk e.limited in scope and size

f. requiring high level management f. small team, minimum supervision

g. too many disparate parts g. seamlessly integrated

h. global reach through relationship h. real time inter-networked

k. no matching engine k. built-in

Specific Issues

a. Netting a. Distributed Node allows reporting of all transaction

b. Risk management b. Any algorithm /real-time mark-to market

- c. Cross product margin c. Inter-connected Nodes are product specific

Sunday, August 26, 2012

Saturday, August 25, 2012

Open Clearing Network System

Open Clearing Network System

An enhanced electronic cash management processing system for financial clearing, linked to banking payment systems, that collectively performs funds movement management, matching and an intelligent routing between any two trading facility. Such system provides continuous clearing and settlement. The system additionally provides an auxiliary processor generating physical delivery receipt against cash settlement. The system further provides frequent marked-to-market pricing data to permit risk management based on margin calculation.

Open Clearing System incorporates standard cash management service to broker's clients which includes a full capability of short- and long-term investments, Automatic sweeps of cash deposit balances to interest-bearing, FDIC-insured bank deposits, control of funds to and from fiduciary account including Fed Wire, access to the account information and transactions 24/7.

The Implementation

The Nodes or trading facility maintains a segregated customers' Fiduciary accounts at designated local banks. Fiduciary account deposits are tagged to an individual identifier ( pin). The Fiduciary account acts as a common settlement account that allows the Escrow account to withdraw from or deposit to at any time. A two way fund transfer from Fiduciary account to an Escrow account allows the Escrow account act as a matching processor.

The designated local commercial bank is a Partner provided the bank support ACH as well as open network of S.W.I.F.T communicating with any local bank that would support conversion formats for transferring funds for cross border clearing.

Clearing and Settlement

CLEARING AND SETTLEMENT IN CAPITAL MARKETS

Industry standards and practices:

Clearing refers to settling claims of one entity ( representing clients) against another. Each entity's operation is responsible for its handling or overseeing the clearing and settlement processes. The processes involve two primary tasks:

i) trade matching and

ii) settlement(physical delivery of securities or book entry).

a) For the simple case of cash market trade execution, buyers and sellers record trade details. Brokers and dealers receive confirmations that the trade has been executed and pass on details of the confirmation to clients. Trade comparison is the second step in the clearing process. Trades are said to be cleared when the buy and sell side records coincide.

b) Such clearing procedure does not specifically address the issue of how the price of, for example, a particular stock is determined. It merely matches the amount of dollar given against the number of shares as the brokers submit.

c) In the case of time-sensitive contract such as options, forwards and futures the pricing is subjected to continuous change. Generally, the method of bid and ask in pricing defines a degree of transparency that minimizes the “spread” between what market participants (floor brokers) expect to pay and or receive as seller.

2. Cost of clearing:

Cost of matching includes the charge imposed by clearing member plus the exchange's Clearinghouse fees. The latter are classified as follows:

a) For typical commodity,( crude oil, NYMEX per contract), ranging from $0.45-$3.00

b) For equities, based on # of shares, fees range from $0.01 to $0.03, one way, for lot (100) shares of stocks. DTC, US stock market clearinghouse, additionally charges for the type of trade, i.e., the ratio of buy and sell.

Cost of settlement

a) cost of settlement/ cash offset usually not advertised, due to various factors. For simple settling full amount of cash against number of shares allocated it ranges from $2 to $5 depending on trade activity and number of shares.

b) cost of delivery of stocks varies from $10 for Direct Registration System to $500 actual certificate issued.

Subscribe to:

Comments (Atom)